This week, construction steel inventory shifted from a decline to an increase. Total rebar inventory stood at 6.1434 million mt, up 1.65% WoW, while total wire rod inventory was 1.2248 million mt, up 3.73% WoW. On the supply side, blast furnace steel mills continued to have profit margins in producing construction materials this week, with moderate production willingness, maintaining normal production levels. However, EAF steel mills faced poor profitability and weakening demand, leading some electric furnace plants in South China to reduce their operating hours. Additionally, some electric furnace plants in Central and South-West China underwent temporary maintenance due to raw material procurement issues, resulting in a slight overall decline in supply. On the demand side, during the Labour Day holiday, cargo transportation was hindered, and construction activities in some regions were temporarily suspended. Subsequently, rainfall and flooding occurred in South China, further impeding construction progress at construction sites. Overall demand performance was average.

This week, total rebar inventory was 6.1434 million mt, increasing by 99,600 mt or 1.65% WoW (previous value: -7.83%). Compared to the same period of the previous lunar year, it decreased by 1.5725 million mt, down 20.38% YoY (previous value: -26.66%).

Table 1: Overview of Rebar Inventory

Data source: SMM

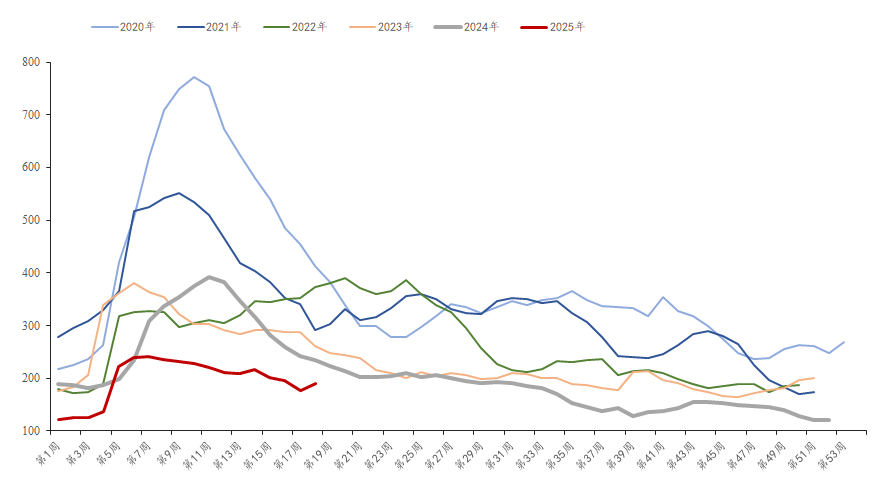

This week, in-plant rebar inventory was 1.9073 million mt, increasing by 151,000 mt or 8.60% WoW (previous value: -9.78%), and decreasing by 228,000 mt or 10.68% YoY (previous value: -21.08%). Due to the downward shift in the price center of rebar futures and spot prices after the holiday, and the strong wait-and-see sentiment in the market amid macro policy disruptions, the overall enthusiasm of agents for picking up goods was low. As a result, in-plant inventory accumulated, and inventory pressure increased.

Chart-1: Overview of Rebar Factory Inventory Trends from 2020 to 2025

Data source: SMM

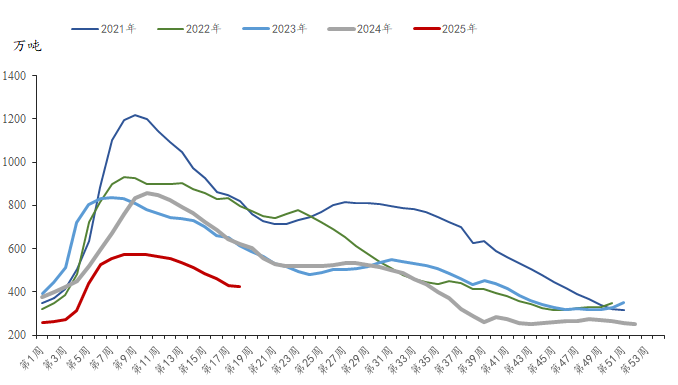

This week, social rebar inventory was 4.2361 million mt, decreasing by 51,500 mt or 1.20% WoW (previous value: -7.01%), and decreasing by 1.3445 million mt or 24.09% YoY (previous value: -28.72%). During the holiday, transportation was hindered, and downstream reserve inventory continued to be consumed. After the holiday, there was some restocking behavior downstream, leading to a continuous reduction in overall social inventory.

Chart-2: Overview of Rebar Social Inventory Trends from 2021 to 2025

Data source: SMM

Looking ahead, on the supply side, there is a divergence in profits between long-flow and short-flow steel mills. Blast furnace steel mills still have profit margins in producing construction materials and are expected to resume production according to their maintenance schedules while also replenishing specifications. According to the SMM survey, the production schedule for construction materials at steel mills in May is expected to increase slightly. EAF steel mills, however, face poor profitability and difficulties in collecting scrap, with electric furnace plants shortening their operating hours and halting production. Overall, the supply of construction materials may increase slightly. On the demand side, downstream construction speeds are expected to gradually recover after the holiday, with a high probability of a wave of demand release. It is expected that construction steel inventory may shift from an increase to a decrease next week, but the overall de-stocking speed will slow down.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)